Find the right interest free payment option for you

At Amart, there are several interest free payment options that let you buy what you want now and pay for it over time.

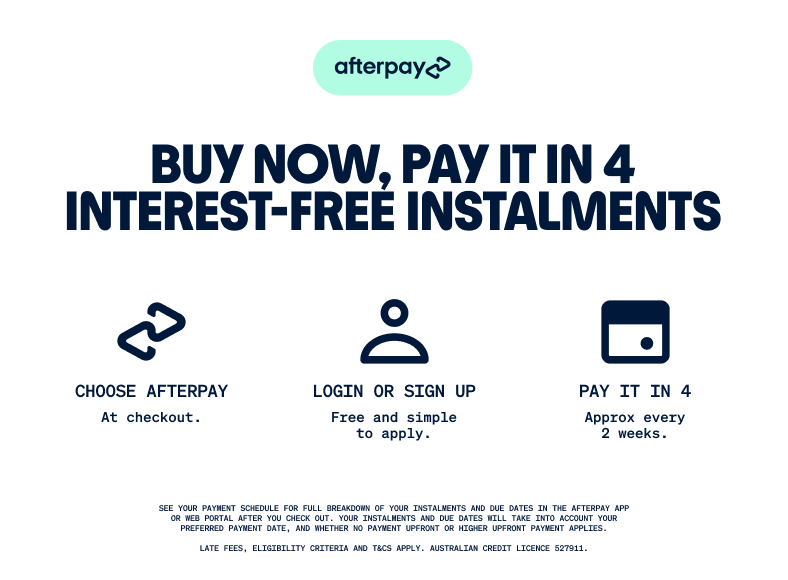

AVAILABLE ONLINE & IN STORE

Shop now, pay it in 4 with Afterpay.

At Amart, you can buy now and pay it in 4 interest-free instalments over 6 weeks.

How does it work?

To set up an Afterpay account you’ll need to:

- Live in Australia or New Zealand

- Be over 18 years of age

- Have an Australian/New Zealand debit or credit card

- Have a valid and verifiable email address and mobile number

- Be capable of entering into a legally binding contract

- Credit checks apply For full terms and conditions visit www.afterpay.com/terms

How does Afterpay work?

When you use Afterpay, you pay for your items in 4 instalments over 6 weeks, without incurring any interest. To use Afterpay, add items to your shopping cart then select Afterpay from the available payment options. You pay for the first instalment of 25% at the time of purchase, and the remaining three instalments will be automatically deducted from your nominated debit or credit card over the following six weeks.

Terms of Service - Australia

LAST UPDATE: 19 June 2025

HIGHLIGHTS:

- Afterpay allows you to pay for a purchase from Retailers and Third Party Suppliers over 4 repayments, payable on the Due Dates outlined in your Payment Schedule. In some cases, Afterpay may require you to make an initial payment at the time of purchase.

- All Orders are subject to Afterpay’s approval – for example, if you have any overdue payments, Afterpay will suspend access for further purchases. For more information on assessment and checks, see clause 8.

- All orders are subject to Afterpay’s approval – for example, if you have any overdue payments, Afterpay will not be available to you. For more information on assessment and checks, see clause 6.2

- You may make early payments, otherwise Afterpay will automatically process payments in accordance with the Due Dates stated on your Payment Schedule. If a payment is not processed on or before the Due Date, Late Fees will apply.

- The following Late Fees apply to the extent that the sum of all Late Fees payable under the Credit Contract and each other Low Cost Credit Contract between Afterpay and you is equal to or less than the Maximum Late Fee Cap:

- For each Order of $40 or below, one Late Fee capped at 25% of the Original Order Value.

- For each Order with a value above $40, an initial Late Fee of $10, and if the payment remains unpaid 7 days after the Due Date, a further Late Fee of $7, up to the lower of 25% of the Original Order Value or $68. We may charge partial amounts to remain within any applicable Late Fee cap.

- Some features accessible on the App may not be accessible on the Web Portal, and vice versa.

- If you won’t be able to pay us on time, please contact us as soon as possible. Please click here for more information regarding Hardship.

- The goods and services and all refunds are the responsibility of the Retailer where you make the purchase or the Third Party Supplier who supplies the Third Party Goods available through our Platforms.

- If you decide to purchase goods from a Retailer from outside of Australia, we draw your attention to clause 5.3.

- We are a Code Compliant Member under the BNPL Code. You have certain rights and we have certain obligations to you under the BNPL Code. For further information, see clause 2.6.

- We limit our liability to you in accordance with clause 13.3, and you indemnify us in accordance with clause 13.4.

The Credit Contract comprises:

- the Schedule;

- these General Terms; and

- the Specific Terms (if any).

Please read these documents carefully as they set out your rights and obligations in respect of your use of the Credit Contract. You are bound by the Credit Contract as soon as you accept it.

The Schedule is the pre-contractual disclosure statement required by the National Credit Code.

You acknowledge that once you download the Afterpay App to your mobile device, or access Afterpay’s Website or Web Portal, these General Terms (to the extent applicable) apply to your use of our Platforms whether or not you have accepted the Credit Contract or placed an Order.

You should keep the Credit Contract for your records, noting that it may be amended from time to time. The latest version of the Terms are available on our Website.

Please also read our Privacy Policy, which includes our Credit Reporting Policy and is available on our Website.

1.1 Nature of the contract

The Credit Contract is a Low Cost Credit Contract and is between you and Afterpay.

1.2 Unilateral changes

(a) We may change the Credit Contract at any time (including changing the amount, frequency or time for payment of Fees and repayments, or imposing new Fees) without your consent. We will only change the Credit Contract for the following reasons:

(i) if we change the functionality of the Afterpay Account in a way that impacts the Credit Contract;

(ii) if we introduce new products or remove existing products or features that impact the Credit Contract;

(iii) where required by law or regulation or by a regulator, or to comply with any change or anticipated change in any relevant law, code of practice, guidance or general good practice;

(iv) to reflect a change in our systems or procedures, including for security reasons;

(v) to make the Credit Contract clearer; or

(vi) for any other reason determined by Afterpay, acting reasonably and having regard to its legitimate business interests.

(b) We will notify you of the change in accordance with this table.

| Type of change | Minimum notice period | Notice method |

|---|---|---|

| Introducing a new Fee or increasing an existing Fee | 20 days | See clause 11. |

| Any change which increases your obligations (or does not change your obligations) | 20 days | |

| Any change which reduces your obligations (or extends the time that you must pay us under a Payment Schedule) | Before or when we provide you with the next account statement |

(c) If you do not wish to be bound by a change, you can close your Afterpay Account before the change takes effect without penalty or additional fees. You cannot close your account until you have paid all outstanding amounts owed to us in full. See clause 11 for how we will communicate with you when giving notice.

(d) We will not change the terms of the Credit Contract as they apply to an existing Order that has been accepted by us without your agreement. The terms that will apply to an accepted Order (and to any steps taken in relation to such Order, e.g., cancellation, refunds, etc.) are the terms that applied at the time you made the Order unless the Credit Contract is changed by agreement with you.

1.3. Agreed changes

We may change the Credit Contract by agreement with you. We will give you a written notice setting out the details of the change within 30 days of the date of the agreement unless the agreed change:

(a) defers or reduces your obligations for a period which is 90 days or less; or

(b) is an increase to your Spend Limit.

2.1. About us

(a) The facility under the Credit Contract allows you to buy:

(i) goods or services offered by Retailers including, if permitted by Afterpay, a Retailer in an overseas jurisdiction; and/or

(ii) Third Party Goods.

(b) By placing an Order (or, in the case of a Recurring Payment, authorising an Order to be placed) with a Retailer or for Third Party Goods, you provide us with an unconditional and irrevocable consent and direction to pay (or at our discretion, to procure Related Party to pay) the Retailer or Third Party Supplier (as applicable) on your behalf, in respect of the Order:

(i) the First Instalment, where it is payable by you at the time of completing the Order; and

(ii) in exchange for your agreement and obligation to repay or pay to us the remaining repayments specified in the Payment Schedule plus any applicable Fees including Late Fees (if any) which are due and payable, in accordance with the Credit Contract, the payments for an Order as specified in your Payment Schedule, which includes the First Instalment where it is not due on completion of the Order (and which may include any applicable taxes, duties or other related amounts charged by the Retailer or Third Party Supplier (as applicable)).

(c) You acknowledge that we do not have any control over, and neither Afterpay nor any of our Related Parties are responsible or liable for the products or services you purchase from Retailers by placing an Order. We cannot ensure that a Retailer or Third Party Supplier you are dealing with will complete the transaction.

(d) You acknowledge that we act as an agent for the Third Party Suppliers when we process Orders for Third Party Goods. Delivery, fulfilment and customer support for the Third Party Goods will be provided by the Third Party Supplier. You agree to be bound by the terms and conditions of the Third Party Supplier identified to you at the time of purchase. Please review all applicable Third Party Supplier terms and conditions prior to placing your Order for any Third Party Goods.

(e) Afterpay does not:

(i) enter into a partnership, joint venture, agency (except as set out above in this clause 2.1) or employment relationship with you;

(ii) guarantee the identity of any Retailer;

(iii) guarantee the performance or delivery of the goods or services by any Retailer or Third Party Supplier;

(iv) determine if you are liable for any taxes; or

(v) collect or pay any taxes on your behalf that may arise from your use of the Afterpay Account.

(f) You acknowledge and agree that some or all of Afterpay’s obligations under the Credit Contract may be performed by one or more of our Related Parties from time to time.

2.2 Your Consumer Rights

(a) As a consumer, you have certain rights under consumer protection legislation (“Consumer Rights”). These Consumer Rights include:

(i) statutory guarantees under the Australian Consumer Law that goods will be of acceptable quality, match their description and be fit for any purpose made known to the consumer, and that services supplied will be provided with due care and skill and be reasonably fit for any specified purpose. When a statutory guarantee is breached, consumers are entitled to a range of remedies including, in some cases, damages for reasonably foreseeable losses; and

(ii) non-excludable implied warranties that financial services will be provided with due care and skill and that the services and any materials supplied in connection with them will be fit for any specified purpose.

(b) Nothing in the Credit Contract is intended to exclude, restrict or modify any of your Consumer Rights, including by limiting our liability or imposing liability on you in a manner which would be considered unfair under the relevant consumer protection laws.

2.3. No warranty

(a) We do not give any express warranty or guarantee as to the suitability, reliability or availability of your Afterpay Account, or Third Party Goods, or of the content on our Platforms.

(b) Subject to your Consumer Rights set out in clause 2.2, we do not give any implied warranties or guarantees.

(c) Except as required by law, we do not guarantee continuous or uninterrupted access to your Afterpay Account, and we make no representations or warranties regarding the amount of time needed to complete processing of Orders or payment transactions. We will take reasonable steps within our control to keep your Afterpay Account secure, but subject to this obligation and except as required by law, we do not guarantee secure access to your Afterpay Account.

2.4. Transfers or assignments

(a) You cannot transfer or assign any rights you may have under the Credit Contract without our prior written consent, which must not be unreasonably withheld.

(b) We may transfer or assign all or any of our rights under the Credit Contract, to a third party without notice to you or your consent unless the assignment will detrimentally affect your rights under the Credit Contract (in which case we will seek your consent prior to the transfer or assignment, which consent must not be unreasonably withheld). We will notify you in writing as soon as reasonably practicable if it is reasonable to do so. You agree that we may appoint third party collections agencies to collect any amounts owing to us under the Credit Contract.

2.5. Appointment of nominated persons

(a) You can nominate a person to receive notices (including hardship notices), make payments to us on your behalf, and to access (but not place Orders with) your Afterpay Account.

(b) Once we have identified you as we reasonably require, you must complete our nomination form and/or provide documentary evidence satisfactory to us of the nomination as set out in clause 2.5(a). Until this clause 2.5(b) has been satisfied, an effective nomination has not been made and we will continue to contact you about your Afterpay Account.

(c) We can, acting reasonably having regard to our obligations at law and under any applicable code, refuse to accept any instructions from any nominated person.

(d) You can contact us to remove a nomination at any time.

2.6. Your rights under the BNPL Code

(a) We are a Code Compliant Member under the BNPL Code. The BNPL Code describes contractually enforceable commitments that apply to the interactions and arrangements we have with you about your Afterpay Account that may be covered by the BNPL Code.

(b) The BNPL Code operates alongside, and is subject to, existing laws and regulations and does not limit your rights under such laws and regulations. Where the BNPL Code imposes standards on us that are above those required by the law or regulation, we are committed to the higher standards of the BNPL Code.

(c) As a Code Compliant Member, we are subject to the oversight of the CCC and our commitments to you under the BNPL Code are enforceable by you through AFCA. For information about raising a complaint with us, AFCA or the CCC – see clause 10.2.

3.1. Your Spend Limit

Your Spend Limit is the "Afterpay BNPL Credit Limit" as specified in the Schedule as varied from time to time in accordance with the Credit Contract. This is the maximum amount of credit that we agree to provide to you under the Credit Contract.

3.2. Spend Limit increases

(a) You consent and agree to us periodically assessing your eligibility for Spend Limit increases, and where we have assessed you as being eligible, you consent to the increase in your Spend Limit by the amount assessed by us in our discretion acting reasonably as notified to you.

(b) You can withdraw your consent to Spend Limit increases by contacting our customer service team via in-app messaging.

(c) We may access your credit report via a credit reporting body to support a Spend Limit increase.

3.3. Spend Limit decreases

(a) We may decrease your Spend Limit at any time acting reasonably.

(b) You can set a limit on the total amount that you can spend with Afterpay by creating a Spend Cap which is independent from your Spend Limit. See how to do this in clause 5.7.

(c) You can request a Spend Limit decrease by contacting our customer service team via in-app

3.4. Available to Spend

(a) The amount you have Available To Spend using your Afterpay Account is shown in the App and Web Portal.

(b) When we approve an Order (subject to any adjustment, cancellation or refund applicable to that Order), your Available To Spend will be reduced by the amount of that Order less any First Instalment (including any Higher Upfront Payment) paid at the time of purchase. The amount of any First Instalment (including any Higher Upfront Payment) paid by you at the time of purchase in accordance with these Terms does not form part of the credit we provide to you. Fees due and owing will not be debited to your Balance but will have the effect of reducing the amount Available To Spend by the amount of the relevant Fees due and owing.

(c) When you make payments to us in accordance with your Payment Schedule (other than when you are in a payment arrangement) or you pay Fees due and owing, your Available To Spend will increase by the same amount (up to your Spend Limit).

(d) Any payments due and payable by you at the time of purchase or any Fees due and owing by you under the Credit Contract are not debited to your Balance and do not form part of the credit. The Late Fees will be shown in your Payment Schedule (where applicable) and will also show in your account statements as an amount owed to us, however this is for your information only and not because of any adjustment made to the Balance.

4.1. Creating your Afterpay Account

(a) Once your Afterpay Account is created, you will be prompted to choose and enter a secure password, and we may allow you to set up biometric security (for example, face ID) on your device. You may then access your Afterpay Account, using your secure password and / or biometric security (where relevant) on your device. Your password should not be easily identifiable by anyone else. For example, you should not use your birth date, phone number or other personal information or sequential numbers (such as “1234”). You should use different passwords for different electronic services (including, for example, banking services), not disclose your password to anyone else or write it down, and take care when keying in your password to make sure that no one else can see it. You must protect your biometric security and not allow others to use it.

(b) You are responsible for maintaining the security of your Afterpay Account details. We will not take responsibility for unauthorised access and use of your Afterpay Account, unless we have failed to take reasonable steps to prevent such unauthorised access or use, or such unauthorised access or use arises from our negligence, error or system failure. You will not be liable to us where any unauthorised access or use of your Afterpay Account arises which is not caused or contributed to by any act or omission by you, whether directly or indirectly.

(c) If you consider a transaction made using your Afterpay Account was not made or otherwise authorised by you, you should contact Afterpay at help.afterpay.com and we will investigate this as an unauthorised transaction. In the absence of such a request from you, you acknowledge and agree that we will treat any such Order on your Afterpay Account as a valid transaction for the purposes of the Credit Contract.

See how we handle complaints in clause 10.2.

4.2. Your obligations to us as a holder of an Afterpay Account

By holding an Afterpay Account with us, you agree that you must:

(a) pay us all amounts you owe including all applicable Fees associated with your use of your Afterpay Account;

(b) not provide us with any information that is false, inaccurate or misleading (including, without limitation, in relation to your identity or personal details, or by using an alias or false identity even with the consent of the person whose identity you are using, or seek to establish a fake, untraceable or unverifiable Afterpay Account);

(c) ensure any information about you, including your contact details, is true, current and complete. If your information changes, you must update it through your Afterpay Account via our App or Web Portal;

(d) provide to us in a timely manner all documentation relating to your identity, if reasonably requested by us;

(e) not use your Afterpay Account, any Platform or Third Party Goods for any unlawful, fraudulent or improper activity, including for any experimental, testing or research purposes, or otherwise in a manner for which they have not been designed;

(f) cooperate fully with us to investigate any suspected unlawful, fraudulent or improper activity on your Afterpay Account;

(g) pay any taxes that may apply to purchasing the goods or services where applicable (e.g. GST);

(h) not permit others to use your Afterpay Account, or allow anyone else to have or use your account password details;

(i) not use any technology (device, software or hardware) to damage, intercept or interfere with your Afterpay Account, or any Platform;

(j) immediately contact us if you believe that your Afterpay Account may be subject to an unauthorised transaction, account takeover or other type of fraudulent activity or security breach;

(k) not create liability for us or any of our Related Parties (excluding our liability to pay a Retailer or Third Party Supplier from your use of your Afterpay Account) or cause us to lose (in whole or in part) the services of our Retailers or Third Party Suppliers through your wrongful acts or omissions;

(l) authorise us to disclose Card-related profile and purchase behaviour information to third parties (including, without limitation, Visa and MasterCard) for the purpose of eliminating fraud and illicit behaviour;

(m) not open or use more than one Afterpay Account;

(n) if you think that you won’t be able to pay us on time, contact us as soon as possible; and

(o) ensure that you update your App software to ensure it is using the latest version. You can find information on the latest version of the App on the App Store or Google Play Store. You must also ensure that your device you use to access any Platform has adequate security, including for example by using a secure internet connection, ensuring that your device is using the latest security release for your hardware and relevant software and you have reasonable anti-virus software and / or protection.

4.3. In-store payment

(a) To make an in-store purchase with a Retailer, you must have added your Afterpay Card to your digital wallet. See our App or Website for instructions. The Afterpay Card cannot be accessed through the Web Portal.

(b) You can place an Order by using your Afterpay Card to finalise your Afterpay purchase with the Retailer at the Retailer's terminal. If we approve the Order, your First Instalment will be due at the time of purchase or, if you have access to and have activated the No Payment Upfront Feature, on the date set out in your Payment Schedule. The First Instalment payment will be deducted from your Selected Payment Method that applies under your Payment Schedule.

(c) Only one Afterpay Card will be approved for your use and can be used to place Orders in-store until its expiry date.

(d) Your Afterpay Card must only be used by you as the Afterpay Account holder. It is your responsibility to keep your Afterpay Card secure at all times from theft, fraud, misuse and/or unauthorised use.

(e) If you become aware that your Afterpay Card is faulty, or the device onto which it has been loaded has been lost or stolen prior to its expiry, or there are issues with generating the Afterpay Card, you can contact us via the App or on help.afterpay.com. If your device is lost or stolen and you contact us, we will deactivate the Afterpay service on your Afterpay Account, meaning that no new Orders, Spend Limit increases or changes to personal details can take place. We will continue to draw Automatic Payments in accordance with your Payment Schedule so that you do not fall behind on your payments. To reactivate your Afterpay Account on your new (or located) device, please contact us again and we will help you with the set up.

(f) To the extent permitted by law, and subject to clause 2.2, neither Afterpay nor any of its Related Parties will be liable to you or anyone else for any losses suffered or incurred due to lost or misdirected Afterpay Cards, or delay in receipt of, or for any failure to generate or provide the Afterpay Cards to the device you have provided, or for any losses suffered or incurred due to the theft, fraud, misuse or unauthorised use of the Afterpay Card, except to the extent that such losses arise as a result of our negligence, wilful misconduct or breach of the Credit Contract.

4.4. Closing your Afterpay Account

(a) We set out information below about you closing your Afterpay Account:

(i) You can ask us to close your Afterpay Account at any time via the App or by contacting us directly and for any reason (including where we are making unilateral changes under clause 1.2) if you have paid all outstanding amounts owed to us (including Fees due and owing) in full.

(ii) If you have outstanding amounts owing to us, you can ask us to deactivate your Afterpay Account so that you cannot place a new Order, and you will be able to ask us to close your Afterpay Account once you have paid all outstanding amounts to us (including Fees due and owing) via the App or by contacting us directly.

(iii) The Credit Contract will continue to apply:

A. to a deactivated Afterpay Account; and

B. where you have asked us to close your Afterpay Account (where you have paid all outstanding amounts owed to us) but you have any unresolved refunds or disputes with the Retailer or the Third Party Supplier.

(iv) Your Afterpay Account will only be closed and the Credit Contract terminated once you have paid all outstanding amounts to us, all disputes have been resolved and all refunds processed.

(b) We can limit access to, suspend, deactivate or close your Afterpay Account as follows:

(i) We may immediately limit your access to, suspend (including suspending your ability to make any new Orders), deactivate or close your Afterpay Account, without prior notice to you, for any of the following reasons:

A. we reasonably consider it necessary to do so in order to protect the integrity of our systems or your Afterpay Account, prevent fraud or limit the risk of money laundering or terrorism financing, or otherwise protect us against any legal, regulatory or non-payment risk (whether at an Afterpay Account level, portfolio level or part of portfolio level);

B. we are required to or instructed by a regulator, enforcement officer or court of law;

C. you do not pass our verifications or checks;

D. you fail to make any payment due under the Credit Contract by the payment Due Date;

E. you provide us with false, inaccurate or misleading information;

F. we reasonably suspect, or are aware that your use of the Afterpay Account or an act or omission made by you is in breach of the Credit Contract;

G. you withdraw (or purport to withdraw) any consent that is integral to our ability to provide your Afterpay Account (for example our ability to provide notices and communicate with you electronically); or

H. we reasonably consider that your Afterpay Account is no longer suitable for you.

(ii) We will use our reasonable endeavours to provide a notice of any suspension prior to or as soon as reasonably practicable after any suspension, unless it is in our legitimate interest not to provide notice. If we close your Afterpay Account without prior notice, we will provide notice that we have done so as soon as reasonably practicable after the closure.

(iii) Other than as set out in clause 4.4(b) above, we may close your Afterpay Account at any time for any reason by providing you with 60 days’ prior notice. For how we give notice, see clause 11.

(c) The Credit Contract will continue to apply to any Order we approve prior to closure (whether it is immediate or with prior notice) until all amounts owing (including Fees) are received in full and until all disputes and refunds are resolved/processed – see clause 7.

5.1. Order confirmation and Payment Schedule

(a) All Orders are subject to approval by Afterpay, in our reasonable discretion. We may choose not to approve an Order or may cancel an approved Order before the goods or services are delivered or supplied, if:

- we reasonably consider this necessary in order to:

- protect the integrity of our systems or any Afterpay Accounts;

- prevent fraud;

- limit the risk of money laundering or terrorism financing; or

- otherwise protect us against legal, regulatory or non-payment risk (whether at an Afterpay Account level, portfolio level or part of portfolio level);

- we enter into a payment arrangement with you as a result of Hardship;

- you do not pass our verifications or checks, including re-verification or those described in clause 8;

- we reasonably suspect, or are aware, that you have breached the Credit Contract in a material respect (including by failing to make any payment due under the Credit Contract on the payment Due Date);

- we reasonably consider that the Afterpay Account is no longer suitable for you;

- we have otherwise limited your access to, suspended, deactivated or closed your Afterpay Account in accordance with the Credit Contract; or

- we otherwise reasonably consider the Order to be suspicious.

(b) If we cancel an approved Order:

- we will provide you with a notice confirming that your Order is cancelled;

- we will pay a full refund of any amounts you have paid to us to your Selected Payment Method for that Order, or where you had more than one Selected Payment Method, to one or more of those Selected Payment Methods we choose. If that is not possible, we will apply the refund to any other Card that you have provided us details of, and will cancel any future payments related to that Order. In the event the approved Order is cancelled because a chargeback has been incurred by Afterpay in relation to a payment by you to Afterpay for the approved Order, that payment will not be refunded by Afterpay. Any return of funds to you in that event will be as between you and the issuing bank of your Selected Payment Method for the Order. The Retailer or Third Party Supplier (as applicable) will not be obliged to deliver the goods (or provide the services) the subject of the Order, unless required to do so by law;

- you will have no obligation to make any further payments to us, or have any other ongoing relationship with us, with respect to that Order; and

- if you wish to proceed with the purchase from the Retailer, the Retailer may accept an alternative way to pay at its discretion, or if required to do so by law.

(c) Once we approve your Order, we will display your Payment Schedule in the App and on the Web Portal. We may also send you an email to the email address you have registered with your Afterpay Account with confirmation of receipt of your Order, payment of the First Instalment (where it is payable at the time of the Order) and the Payment Schedule.

(d) You acknowledge and agree that in an Order we approve may be adjusted to reflect the amount you agree to pay the Retailer or the Third Party Supplier in respect of the Order, and when this occurs it will be taken as a request by you that the Original Order Value and the Payment Schedule for the Order, if we agree to your request, the Original Order Value will be adjusted and the Payment Schedule for the Order (including each specified repayment) will be adjusted to reflect the Original Order Value as adjusted. We will notify you of this agreed variation. This may occur whether, for example, the Original Order Value increases because you have authorised this and the Retailer (or the Third Party Supplier) processes the payment after you place the Order, or the Original Order Value decreases because certain out-of-stock items have been removed from the Order and the Retailer (or the Third Party Supplier) processes the adjustment after we approve the Order.

5.2 Repayment and Payment Methods

(a) Your Payment Schedule, in respect of each Order, details the amount you must pay us in respect of the Order and when those amounts are payable. The frequency and method of calculating the amounts and the timing of the amount of the repayments are set out in the Payment Schedule.

(b) Subject to other clauses of these General Terms, you expressly consent to, authorise and instruct Afterpay to:

- process Automatic Payments on your Selected Payment Method for the amounts (including Late Fees, if applicable) that are due and on the Scheduled Due Dates set out in your Payment Schedule or as otherwise due and payable under the Credit Contract.

- process Automatic Payments in aggregate, rather than as individual transactions where there are multiple payments across Payment Schedules under the Credit Contract to be made on the same day.

(c) You may make early repayments (where such payment will be applied to the amounts in your Payment Schedule for an Order as we reasonably determine) but if you do so you will not be able to reschedule those payments if you change your mind. We may, acting reasonably, also apply early repayment you make in payment of other amounts you owe under the Credit Contract. We will apply any early repayment in the following manner, firstly to overdue Late Fees and then to the specified repayments in your Payment Schedule(s). Unless you have paid or agree upon an amount in full by way of early repayment, Afterpay will automatically process payments as set out in clause 5.2(b). If an Automatic Payment is on any Due Date, or we have reasonable grounds to suspect it will fail, you agree that Afterpay may, and you instruct Afterpay to, attempt or re-attempt to process the payment, including at a later time or date using any Payment Method you have provided until the outstanding amounts you owe are paid. There may be restrictions on removing a Payment Method until all amounts you owe have been paid.

(d) You will have the option to select a Preferred Payment Method when your Afterpay Account is being created and this will be pre-selected for any future Orders.

(e) Afterpay may seek payment by way of any of the Payment Methods provided by you. Whenever you add a Payment Method, we will do an account verification check on it. You can update or change any Payment Method at any time via your Afterpay Account or where the option is available, via the Afterpay checkout process. However, you must always have at least one Preferred Payment Method that we have accepted.

(f) You acknowledge that each Recurring Payment will be deemed an Order. When you select Afterpay as your payment method for a Recurring Payment, you authorise Afterpay to be the default way to pay for ongoing Recurring Payments with the Retailer until you inform the Retailer otherwise (subject to the Retailer’s terms and policies). You acknowledge that you are giving us the ability to collect or reverse fixed or variable payment amounts from your Payment Method, in accordance with your Payment Schedule and the Credit Contract.

(g) If you wish to cancel any once-off purchases or subscriptions in respect of goods or services offered by a Retailer that are structured as Recurring Payments, you will be responsible for contacting the Retailer directly to cancel this in accordance with the Retailer’s terms and policies. You cannot cancel any scheduled Recurring Payment without providing at least 2 days of notice after repayment in your Payment Schedule, either through our App or Web Portal. By contacting Afterpay and requesting the scheduled Recurring Payment amount, Afterpay will also cancel any future Recurring Payments you have for goods or services offered by that Retailer to you. You are responsible for any outstanding amounts or obligations imposed by the Retailer in respect of the cancellation of the Recurring Payment. Please note, cancelling your Recurring Payment with Afterpay will not cancel any once-off purchases or subscriptions in respect of goods or services obtained from the Retailer. As above, it is your responsibility to cancel any orders placed for goods or services obtained from a Retailer, and any such cancellation will be in accordance with the Retailer’s terms and policies.

(h) You are responsible for ensuring that you have sufficient funds in your Selected Payment Method or other relevant Payment Method(s) available to make Automatic Payments on the Due Dates. You are liable for any fees or charges imposed by any of your Payment Methods (e.g. interest charges on a nominated credit card), except to the extent that such fees or charges are as a result of error or system failure. If any fees or charges are imposed as a result of error or system failure, please provide us with a copy of the relevant records, and we will reimburse you for the relevant fees or charges.

(i) If an Automatic Payment fails (for example, if your Selected Payment Method is a credit or debit card that has expired), Late Fees may apply unless you otherwise make the scheduled payment on or before the end of the relevant Due Date. You authorise us to satisfy any liability you owe us by:

- debiting your Selected Payment Method at a later time or date;

- debiting any other Card which you have provided details of;

- offsetting the payment amount against any amounts we may owe to you;

- any other legal means.

Please see clause 6.1 below for more information regarding Late Fees.

(j) If, for any reason, including but not limited to a system error, technical failure, or other unforeseen event beyond our control, an Automatic Payment is not processed on the relevant Due Date, we may attempt to process the payment on a later date. You agree that any such later attempt will not be considered a breach of the Credit Contract, and any repayment processed within a reasonable time after the original Due Date will be treated as if made on time, unless otherwise required by law.

(f) If you have access to the No Payment Upfront Feature and do not make your payments when they are due (unless solely due to our error), we may deactivate the No Payment Upfront Feature without prior notice to you. Acting reasonably, we may also deactivate the feature without prior notice to you where we consider that deactivation is reasonably necessary to protect our legitimate interests (which include the commercially reasonable management of your Afterpay Account and the management of certain risks, including the credit, operational and regulatory risks we are exposed to when providing your Afterpay Account to you). If we deactivate the feature, this may be communicated to you and/or we may let you know in the App.

5.3. Cross Border Transactions

Where you use your Afterpay Account to make a Cross Border Transaction, we will convert what the Retailer charges for the goods into your local currency to determine the Original Order Value and the amounts payable by you in accordance with your Payment Schedule at the retail exchange rate used, which is the average of the bid rate offered by the four largest retail banks in Australia.

5.4. Higher Upfront Payment

(a) Where the Original Order Value exceeds your Available to Spend, you may be offered the option to make an initial payment at the time of purchase which is higher than 25% of the Original Order Value (“Higher Upfront Payment”).

(b) If this clause 5.4 applies to your Order, the Higher Upfront Payment will display prior to you confirming your Order, and we will act as your agent by paying through your Higher Upfront Payment to the Retailer as set out in clause 2.1. The Higher Upfront Payment does not form part of the amount of credit provided by Afterpay.

(c) For the avoidance of doubt, your obligations with respect to your Payment Schedule (regardless of the applicability of this section 5.4) shall continue to apply in accordance with these General Terms.

5.5. No Payment Upfront Feature

(a) If made available to you, the “no payment upfront feature” will display in the App and allow you to defer your First Instalment on an eligible Order from the Order date to a later date as set out in your Payment Schedule (“No Payment Upfront Feature”).

(b) An eligible Order for the No Payment Upfront Feature is an Order that Afterpay determines as eligible for the No Payment Upfront Feature in its discretion (having regard to such matters as whether the type of Order including nature of the goods or services, the Retailer and / or the Third Party Supplier meets its risk requirements) and as notified to you when placing an Order.

(c) If we make the No Payment Upfront Feature available to you, the App will show that the feature is active. We may also send you a communication confirming that you have access to the feature.

(d) If we make the No Payment Upfront Feature available to you, you can turn the feature on or off at any time within the Afterpay App, except where you have lost access to the No Payment Upfront Feature in accordance with clause 5.5(f) below, in which case the feature can only be reactivated by Afterpay.

(e) Afterpay will decide, acting reasonably, whether to make the No Payment Upfront Feature available to you and for how long (whether for the first time or in considering whether to reactivate the feature after a deactivation). In deciding these things, Afterpay will consider a range of factors including your use of your Afterpay Account, payment behaviours and tenure.

(f) If you have access to the No Payment Upfront Feature and do not make your payments when they are due (unless solely due to our error), we may deactivate the No Payment Upfront Feature without prior notice to you. Acting reasonably, we may also deactivate the feature without prior notice to you where we consider that deactivation is reasonably necessary to protect our legitimate interests (which include the commercially reasonable management of your Afterpay Account and the management of certain risks, including the credit, operational and regulatory risks we are exposed to when providing your Afterpay Account to you). If we deactivate the feature, this may be communicated to you and/or we may let you know in the App.

5.6 Preferred Payment Day

(a) You may (or, if clause 5.6(d) applies, we may) select your preferred day of the week ("Preferred Payment Day") on which Due Dates in respect of each Order are to fall.

(b) Once the Preferred Payment Day is set, your Payment Schedule for each subsequent Order completed will reflect the Preferred Payment Day, subject to the following:

- A. The First Instalment for an eligible Order will be due on the Preferred Payment Day that falls a minimum of 8 days and a maximum of 14 days after the date of your Order; and

- B. Each remaining repayment will be due fortnightly thereafter, or as otherwise set out in your Payment Schedule.

- A. The First Instalment will be due on completion of your Order;

- B. The second repayment will be due on the next Preferred Payment Day that falls at least 2 weeks after the date of your Order; and

- C. Each remaining repayment will be due fortnightly thereafter, or as otherwise set out in your Payment Schedule.

(i) If you have access to the No Payment Upfront Feature and it is active:

(ii) If you do not have access to the No Payment Upfront Feature:

(c) Once the Preferred Payment Day is set, it will apply only to future Orders. Payments in respect of any existing Orders will continue to be payable in accordance with the existing Payment Schedule, subject to your ability (if any) to change the Due Dates yourself via the App or Web Portal, or any request you make to Afterpay to change the Due Dates, which Afterpay may accept or reject in its discretion.

(d) If you do not select your preferred day when the feature is available, we will default your Preferred Payment Day to a day we choose.

(e) You may amend your Preferred Payment Day for future Orders at any time in the Afterpay App.

5.7 Spend Cap

(a) You can create a Spend Cap in the App. The Spend Cap is independent from your Spend Limit.

(b) You can set a Preferred Spend Cap and can change the amount of your Spend Cap (subject to a minimum and maximum Spend Cap amount, which will show up in the App) and turn it on or off at any time.

(c) If you create a Spend Cap, your Balance together with Fees due and owing will not be able to exceed your Spend Cap.

6.1. Fees

You must pay us Late Fees and any other fees and charges as detailed in and in accordance with the Schedule, and any Specific Terms, as varied from time to time.

6.2. Interest

No interest charges are payable by you under the Credit Contract.

6.3. Commission

The details of any commission paid by us or to us in relation to your Afterpay Account are disclosed in the Schedule (including the amounts where ascertainable).

(a) If you decide to return goods to a Retailer or Third Party Supplier (as applicable), which have been purchased using your Afterpay Account, and request a refund, or a return and refund are otherwise accepted by the Retailer or Third Party Supplier or permitted by law, you will directly arrange the return with the Retailer or Third Party Supplier, ensuring that the goods are returned according to the Retailer’s or Third Party Supplier’s returns policy (or the policies of an online marketplace) or other instructions or your rights at law. Please note, using Afterpay to pay for any eligible purchase will not affect any of your existing rights to refund under applicable consumer law or otherwise.

(b) It is your responsibility to notify the Retailer or Third Party Supplier if you intend to return any goods or request a refund for goods or services. The return or refund must be completed within the period specified and in the manner required by the Retailer’s or Third Party Supplier’s returns policy (or the online marketplace’s policies, if applicable) or as otherwise permitted by the Retailer, Third Party Supplier or by law.

(c) Unless we are notified by a Retailer or Third Party Supplier (or the provider of an online marketplace, if applicable) that a return (if applicable) has been completed and a refund has been issued, we will continue to process any Automatic Payments in accordance with the Due Dates. Late Fees will apply in accordance to the Credit Contract if you miss a payment, even if you are seeking a refund.

(d) Until such time that the Retailer or Third Party Supplier (or the provider of an online marketplace, if applicable) has confirmed the return of the goods or that services have not been provided (if applicable) and has issued a transaction reversal for those goods or services, you will still need to make the payments in accordance with your Payment Schedule.

(e) Once the Retailer or Third Party Supplier has confirmed that a refund is payable, we will issue a refund to your Selected Payment Method for that Order, or where you had more than one Selected Payment Method, to one or more of those Selected Payment Methods we choose (or, if that is not possible, to any other Card that you have provided details of) and/or if there are amounts payable to us in respect of the Order, it will be taken as a request by you to vary the Payment Schedule for the Order to reflect the amount of the refund (by applying the refund amount to the last payment first and then to each preceding payment). If we agree to your request, you agree that the refund amount will be applied to your Afterpay Account, and the Original Order Value and Payment Schedule for the Order (including each specified payment) will be varied to reflect the Original Order Value as adjusted for the refund. We will notify you of this agreed variation. Please note, in the event of a partial refund of an Order, refund amounts are taken off the last payment/s first. If the refund is processed to your expired or cancelled Card, you will need to obtain the refunded funds by contacting your financial institution.

For example, if you make a $400 purchase using Afterpay and the Retailer approves a $250 refund, your 3rd and 4th repayments of $100 will be adjusted to zero, and your 2nd repayment adjusted to $50. Your new Payment Schedule will become 2 payments (instead of 4) of $100 and $50. If you had already paid 2 repayments of $100 each, a refund of $50 would be applied to your Card and the remaining 2 repayments would be adjusted to zero.

When a Retailer issues a refund for a Cross Border Transaction, the original retail exchange rate (used at the time the Order was placed) will determine the refund amount to apply to your Selected Payment Method(s) or to adjust your Payment Schedule for the relevant Order.

For example, if a New Zealand Retailer charged 100NZD which was converted to $96 as the Original Order Value, if the Retailer issues a refund for 50NZD, your Order total and Payment Schedule will be adjusted by $48.

(f) Where you wish to return a product 120 days or more after the purchase date, we will no longer have any involvement in the product return process (e.g. the Retailer will provide any agreed refund directly to you). A longer period will apply where we have agreed to a longer period with a Retailer or Third Party Supplier or online marketplace (as applicable) where required based on the nature of the goods or services purchased by you.

(g) Where your Afterpay Account has been closed for any reason, our respective obligations in relation to product returns in this clause 7 will only continue until the earlier of:

- (i) the date on which all amounts you owe to us have been paid to us; or

- (ii) the date which is 120 days after your last Order or a later date as we have agreed with a Retailer or Third Party Supplier where required based on the nature of the goods or services purchased by you.

After that time, the Retailer, Third Party Supplier or online marketplace (as applicable) will be solely responsible for processing all product returns and associated refunds. If the Retailer, Third Party Supplier or online marketplace (as applicable) refunds any amount through your Afterpay Account, we will issue that amount to what was your Selected Payment Method for the purchase (or, if that is not possible, to any other Card that you have provided details of).

8.1. Assessment

(a) Afterpay has made an election under section 133BXA(1) of the National Consumer Credit Protection Act 2009 (Cth) (“NCCP Act”) that covers this Credit Contract and the election is in force. Afterpay is subject to modified responsible lending obligations under the NCCP Act and is required to take appropriate and proportionate steps to assess the suitability of lending, including before we enter a credit contract or increase a credit limit.

(b) We reserve the right to assess, and determine whether to accept or cancel, each Order in accordance with clause 5.1.

8.2. Repayment capability and identity checks

(a) We reserve the right to verify your identity, including if required under the Anti-Money Laundering and Counter-Terrorism Financing Act. Verifying your identity does not mean we will approve your Order (see clause 5.1(a) for other variables that are considered).

(b) You agree to provide any information or documentation reasonably requested by Afterpay, a Retailer or a Third Party Supplier to verify your identity in connection with your Afterpay Account or Orders.

(c) You authorise us to make, directly or through third parties, any enquiries we consider necessary to verify your identity and assess your capability to make payments in relation to all Orders. This may include performing repayment capability checks, enquiries with credit reporting bodies and verifying information you provide against third party databases.

(d) All information that Afterpay collects about you or the recipient you nominate, including information collected in connection with the verification of your identity, will be collected, used and stored in accordance with the Afterpay Privacy Policy which you can find on our Website.

(e) You authorise Afterpay (or any third parties providing services on behalf of Afterpay) to disclose to third parties, to the extent required or permitted by any applicable laws or regulations, any information in relation to you or your Afterpay Account.

(a) Our Platforms and all content on our Platforms are the exclusive property of Afterpay, Afterpay Affiliates or other third parties such as our partners. With the exception of any information forming part of any agreement between Afterpay and you, the information on our Platforms is for information purposes only and is subject to change without notice.

(b) You must not copy, imitate, modify, alter, amend or use without our prior written consent any URLs representing any Platform, or any of our content, logos, graphics, icons or other content published on our Platforms or in our printed media.

10.1. Disputes between you and a Retailer or Third Party Supplier

(a) If you have a dispute with a Retailer or Third Party Supplier (as applicable), you should file a dispute through direct contact with the relevant Retailer or Third Party Supplier.

(b) In some instances, Afterpay may facilitate communication between you and the Retailer or Third Party Supplier to enable a resolution to the dispute. The outcome of any dispute with a Retailer or Third Party Supplier will not affect Afterpay’s rights and remedies under Credit Contract or your obligation to meet any payments due to us, except as expressly provided in clause 7.

10.2. Complaints

(a) We:

- (i) will acknowledge receipt of all complaints within 1 Business Day or as soon as reasonably practicable;

- (ii) will provide an initial response to all complaints within 10 Business Days from the date of the complaint; and

- (iii) aim to resolve all complaints within 21 days.

(b) If you wish to raise a complaint related to your Afterpay Account, these General Terms or the Credit Contract, you should do so by contacting us via the Help icon in the My Afterpay tab in our App, or on our Website at help.afterpay.com. Complaints against us should be raised with us as soon as possible.

(c) We may request additional documentation from you to assist us in resolving any complaints or disputes, and you must provide all reasonable assistance to us to facilitate us in resolving any complaints or disputes.

(d) Where we cannot resolve a complaint within 21 days, we will notify you of the reason for the delay as well as an indication of when we expect to resolve the complaint or dispute.

(e) When we have completed our investigation of your complaint, we will provide you with a written response, which will include:

- (i) the outcome of our investigation;

- (ii) your right to take your complaint to AFCA; and

- (iii) AFCA’s contact details.

(f) There may be some circumstances where (unless otherwise required to do so) we will not provide a written response to you because we have either:

- (i) resolved the complaint to your satisfaction within 5 Business Days; or

- (ii) given you an appropriate explanation and / or apology and there are no further actions we can take to reasonably address the complaint.

(g) If you are not satisfied with the outcome of your complaint after it has been through our internal disputes process above, you can contact the AFCA using the contact details listed below:

AFCA email: info@afca.org.au

AFCA website: www.afca.org.au

Phone: 1800 931 678 (free call)

In writing to: Australian Financial Complaints Authority GPO Box 3, Melbourne VIC 3001

(h) If you have a specific dispute with us that involves a breach of the BNPL Code, you should contact us in the first instance and then contact AFCA, if considered necessary. AFCA may not deal with your dispute unless you have tried to resolve the problem with us first, and either:

- (i) we have provided you with a formal response; or

- (ii) at least 20 Business Days (or the timeframe outlined by AFCA) has elapsed since you made your complaint.

In addition to contacting us or AFCA, you can report an alleged breach of the BNPL Code to the CCC. The CCC will not consider your complaint if you are still trying to resolve it with us, or with AFCA. To lodge a complaint with the CCC, you can contact them at CCC-BNPL@afia.asn.au.

10.3. Hardship

(a) If you tell us you have or are likely to have difficulty making payments due in respect of your Afterpay Account, this will be an application for Hardship ("Hardship Application").

(b) While considering your Hardship Application, we may ask you for more information.

(c) If you make a Hardship Application, and we do not receive adequate information about your Hardship, or we do not agree with your proposal on how to change the Credit Contract, you agree to any changes we make to the Credit Contract to provide you with a "payment holiday" (e.g. a deferral of one or more Due Dates).

11.1. How we will communicate with you

(a) These General Terms and any other terms, agreements, notices or other communications regarding your Afterpay Account will be provided to you electronically, unless otherwise required by law.

(b) We may give you notice by:

- (i) sending it to you via electronic methods of communication using contact details listed on your Afterpay Account (including email and short-messaging services (SMS) text messages); or

- (ii) making it available via any other information system.

(c) Where a notice is sent by email, or through other electronic means, service of the notice is taken to be effected on the day on which it is sent, unless we receive notification that delivery has failed.

(d) You must ensure that your email address remains up to date and can receive emails, and you must check the Afterpay App regularly as email is one of the primary ways we communicate with you.

(e) You consent to us using the most recent contact details you have provided to us to:

- (i) contact you on an ongoing basis for marketing purposes whether by email, SMS, push notifications, phone or otherwise (unless you have notified us that you do not wish to receive such communication); and/or

- (ii) contact you in relation to your Afterpay Account and/or any Third Party Goods you have purchased.

(f) You acknowledge that if you withdraw consent to electronic communications, we may continue to send you messages via electronic communication where necessary solely for administrative or customer service purposes.

(g) You acknowledge that we (or any third party providing services on behalf of us) may monitor or record telephone conversations or electronic communication for quality control and training purposes or for Afterpay’s own protection. Afterpay does not provide any guarantee that any such monitoring or recording will be retained or retrievable.

(h) We may also provide notice in other ways, including by way of push notifications, pop-ups or banners, in the App, Web Portal or Website.

11.2. How you can communicate with us

If you wish to contact us for any reason, you can do so using the details in the App, including by email to info@afterpay.com.au.

12.1. General

(a) Except where clause 12.1(b) applies, we will give you an account statement at the frequency set out in the Schedule by notifying you that your account statement is accessible in the Afterpay App, or how you may otherwise access your account statement.

(b) We may choose not to give you an account statement where:

- (i) for the statement period, no amount has been debited or credited to your Afterpay Account during the period and the closing balance is less than $10;

- (ii) Afterpay waived the debt during the statement period and no further debits or credit have been made to your Afterpay Account;

- (iii) you have committed a default at any time in the last 2 months preceding the statement period, and Afterpay has exercised a right not to provide further credit under the Credit Contract; or

- (iv) you die or become insolvent, and your personal representative or trustee in bankruptcy has not requested an account statement.

(c) Your account statement will show the amounts debited and credited to your Balance.

(d) For completeness, your account statement may also show amounts that are not credited or debited to your Balance, such as repayments due at the time an Order is placed and fees that are charged to any Payment Method you have given us. These are included for your information.

(e) Generally, amounts debited or credited to your Afterpay Account or Balance (as relevant) will take effect on that date the debit or credit is processed (which, in the case of a credit, will be as soon as practicable after receipt). However, if a manual payment to Afterpay is made by you, or on your behalf, the date we process the payment will be the date we match it up to your Afterpay Account rather than the date the manual payment was received.

12.2. Checking your statements

You should check your account statement as soon as you receive it and report any suspected unauthorised transactions or errors to us at help.afterpay.com for our investigation.

13.1. System outages and access

(a) Access to your Afterpay Account or any Platform may occasionally be unavailable or limited due to hardware or software failure or defects, overloading of system capacity, damage from natural events or disasters or disruptive human activity, interruption of power systems, labour shortages or stoppages, legal or regulatory restrictions as well as other causes outside of our reasonable control.

(b) To the extent permitted by law, and subject to clause 2.2, neither Afterpay nor any of its Related Parties will be liable for any loss or damage which you may incur as a result of your Afterpay Account or any Platform being unavailable.

(c) Some features accessible on the App may not be accessible on the Web Portal, and vice versa.

13.2. Governing law and jurisdiction

(a) The Credit Contract is governed by the law in force in New South Wales, Australia.

(b) Each party irrevocably submits to the non-exclusive jurisdiction of courts exercising jurisdiction in New South Wales, Australia.

13.3. Limiting our liability to you and your liability to us

(a) Nothing in the Terms is intended to exclude, restrict, modify or limit your rights under your Consumer Rights.

(b) Our liability to you when statutory guarantees and non-excludable implied warranties do not apply is limited as follows:

- (i) Save as set out in clauses 13.3(b)(ii) and 13.3(b)(iii) below, our liability for all claims arising under or related in any way to the Credit Contract and your Afterpay Account no matter how arising, and whether in contract, tort (including negligence), or otherwise, will not exceed the total value of any affected Order(s), including any payments and Late Fees.

- (ii) Subject to clause 13.3(c)(iii), neither we nor any of our Related Parties, or any third party providing services on behalf of Afterpay, and the directors, employees, officers, agents and representatives of them, are liable to you for any loss or damage (including any direct loss or damage or Consequential Loss) you or any third party may incur from your purchase or use of any goods or services from a Retailer or a Third Party Supplier, or from your use of an online marketplace. You acknowledge that this is a matter between you and the Retailer or Third Party Supplier, subject to any obligation on us to process refunds and cancel future payments in accordance with these General Terms and our agreement with the Retailer or Third Party Supplier.

- (iii) Neither we nor any of our Related Parties are liable to you to the extent that your acts or omissions cause or contribute to the loss or damage or where you fail to take all reasonable steps to mitigate the loss arising.

(c) Your liability to us

- (i) See clause 13.5 for your liability to us where you misuse your Afterpay Account.

- (ii) Subject to clause 13.3(c)(iii) below, your liability to us for all claims arising under or related in any way to the Credit Contract no matter how arising, and whether in contract, tort (including negligence), or otherwise, will not exceed the total value of any affected Order(s), including any payments and Late Fees.

- (iii) You are not liable to us where our acts or omissions (or the acts or omissions of our Related Parties, any third party providing services on behalf of Afterpay, or the directors, employees, officers, agents and representatives of them) cause or contribute to the loss or damage or where we fail to take all reasonable steps to mitigate the loss arising.

13.4. Liability

(a) You are liable to Afterpay for any loss, costs (including reasonable legal fees), expense or damage suffered or incurred by each Indemnified Party to the extent they are involved in the provision of the Afterpay Account:

- (i) in connection with any claim or demand made by any third party due to or arising out of your breach of the Credit Contract, or your breach of any law or of the rights of a third party relating to your use of our your Afterpay Account or Website; and

- (ii) as a direct or indirect consequence of unauthorised users accessing your account as a result of your negligence.

(b) Your liability under clause 13.4(a) will be reduced proportionately to the extent that any Indemnified Party:

- (i) caused or contributed to the relevant claim, demand, loss or damage; or

- (ii) failed to take reasonable steps to mitigate the relevant claim, demand, loss or damage.

13.5. Breach relating to misuse of the Afterpay Account

(a) You acknowledge that it is imperative that Afterpay be able to rely on:

- (i) the information you provide to us;

- (ii) the identity that you use; and

- (iii) that your use of your Afterpay Account be for the intended purpose.

(b) You acknowledge that a breach by you of any obligation in these General Terms in relation to the matters in clause 13.5(a) (including, without limitation, a breach of clauses 2.4 or 4.2(b) and/or 4.2(e)) that is in substance material, would cause significant detriment to Afterpay and/or its Related Parties. You agree that monetary damages will not be sufficient to remedy that detriment, or may otherwise be incapable of being ascertained, and irrevocably consent to Afterpay or any of its Related Parties seeking and obtaining injunctive relief to obtain relevant documents from you and to prevent such breach, or orders of specific performance to compel compliance, in addition to any other remedies available at law or in equity.

(c) If Afterpay reasonably considers that you have breached an obligation under the Terms in relation to your identity, the information you provide to us and/or your use of your Afterpay Account, you agree, on request from Afterpay, to provide Afterpay with copies of all documents, notes or communications in relation to such alleged breach.

13.6. Survival

This clause 13 survives termination of the Credit Contract.

13.7. No set off

Notwithstanding any other provisions of the Terms, you must pay all amounts you owe us in full to us under the Credit Contract without any set-off, withholding or reduction except to the extent that you have a right of set-off granted by law which Afterpay cannot exclude by agreement or the amounts are the subject of dispute resolution proceedings or court action.

14.1. Definitions

$ means Australian dollars.

AFCA means Australian Financial Complaints Authority - https://www.afca.org.au.https://www.afca.org.au.

AFIA means Australian Finance Industry Association Limited – www.afia.asn.au.

Afterpay, we, us or our means Afterpay Australia Pty Ltd ABN 15 169 342 947, Australian Credit Licence 527911.

Afterpay Account means an account that Afterpay creates and held in your name in respect of the Credit Contract.

Afterpay Affiliate means a related body corporate or related entity of Afterpay, including one in another jurisdiction.

Afterpay App or App means our application downloadable directly to your mobile device from the App Store or Google Play, to access and manage your Afterpay Account.

Afterpay Card means the Afterpay card generated using the Afterpay App (linked to the digital wallet on the device on which it is loaded) and authorised for your use to make your Afterpay purchase in-store or online (where enabled).

Automatic Payment means an automatic payment by you on a one-time or regular basis as set out in the Terms that we will automatically charge.

Available to Spend, at any time, means either:

Balance means the total amount of credit advanced under the Credit Contract that remains outstanding at a given time. For the avoidance of doubt, this excludes amounts owing that are not part of the credit amount (such as Fees).

BNPL Code means the Code of Practice for Buy Now Pay Later Providers that is available at https://afia.asn.au/AFIA-Buy-Now-Pay-Later-Code-of-Practice

Business Day means a day other than a Saturday, Sunday or a public holiday in Victoria, Australia.

Card means any Australian card issued by Visa or MasterCard, excluding Gift Cards and other pre-paid cards.

CCC (or Code Compliance Committee) means the independent committee established by AFIA to monitor and investigate compliance with the BNPL Code.

Code Compliant Member means a member of AFIA that has been approved as a Code Compliant Member by AFIA and is a signatory to the BNPL Code.

Consequential Loss means any loss, damage or costs incurred that is:

Consumer Rights has the meaning given in clause 2.2.

Cross Border Transaction means an Afterpay purchase between you and a Retailer in an overseas jurisdiction permitted by Afterpay.

Credit Contract means the credit contract applying to your use of your Afterpay Account comprising these General Terms, the Schedule and, if any, the Specific Terms.

Due Date means a due date for a repayment in an Order as set out in a Payment Schedule (as amended by us).

Fees means the credit fees and charges set out in the Schedule as amended from time to time in accordance with clause 1.2, including Late Fees.

First Fee Period means the “First Fee Period” set out in the Schedule in Table 2 under the heading “Credit fees and charges”.

First Instalment, in respect of an Order, means the first payment for that Order. We calculate this as a dollar amount or percentage of the Original Order Value. Where clause 5.4 applies, the First Instalment is the Higher Upfront Payment.

Gift Card means a stored value or prepaid card which, when activated:

Hardship means you are unable (or will be unable) to meet your repayment obligations under the Credit Contract.

Hardship Application has the meaning given in clause 10.3(a).

Higher Upfront Payment has the meaning given in clause 5.4.

Indemnified Party means each of Afterpay, its Related Parties, any third party providing services on behalf of Afterpay, and their respective directors, employees, officers, agents and representatives.

Late Fees mean the “Late Fees” set out in the Schedule under the heading “Credit fees and charges”.

Low Cost Credit Contract has the meaning given to it under section 13E of the National Credit Code.

Maximum Late Fee Cap means the “Maximum Late Fee Cap” set out in the Schedule in Table 2 under the heading “Credit fees and charges”.

National Credit Code means the National Credit Code being Schedule 1 of the National Consumer Credit Protection Act 2009 (Cth).

No Payment Upfront Feature has the meaning given in clause 5.5.

Order means a request submitted by you to us, to use your Afterpay Account to (subject to these General Terms where the First Instalment is payable by you at the time of your Order) pay for goods or services offered by a Retailer (whether on the Retailer’s website or at an in-store location of the Retailer) or to pay for Third Party Goods (as is relevant).

Original Order Value means the total cost of your Order before any refunds may be applied, which may be displayed to you when you check out (whether by Afterpay, a Retailer or a Third Party Supplier).

Payment Method means any payment method accepted by Afterpay from time to time, including a Card.

Payment Schedule means:

For the avoidance of doubt, the applicable timezone for all Due Dates provided as part of a Payment Schedule shall be the applicable timezone in Melbourne, Australia.

Platforms means our App, Website and Web Portal, and Platform means any of them.

Preferred Payment Day has the meaning given in clause 5.6.

Preferred Payment Method means the Payment Method you have chosen and nominated as the primary payment method in the App or Web Portal from time to time, which will be pre-selected when you place an Order.

Recurring Payment means each arrangement made between you and a Retailer or Afterpay for your Afterpay Account to be used for any recurring payments, which may also be described by a Retailer or Afterpay as subscriptions, billing agreements, pre-authorised payments, fixed recurring payments, flexible recurring payments or any reasonably similar term.

Related Parties means the Afterpay Affiliates and any directors, officers, employees, agents, representatives or contractors of those Afterpay Affiliates.

Retailer means an online or in-store merchant whose goods or services may be purchased by you using your Afterpay Account.

Schedule means the document titled ‘Schedule’ which contains the financial table and certain other information.

Selected Payment Method means the Payment Method that you have selected for an Order, which you may update from time to time.

Specific Terms means any ‘Specific Terms’ we agree to with you and which supplement these General Terms.

Spend Cap means a self-imposed maximum limit on the total amount that you can spend with Afterpay.

Spend Limit means the credit limit set out the Schedule, or as varied by a subsequent notice to you relating to any limit increase or limit decrease.

Terms means these General Terms and the Specific Terms (if any), as amended from time to time.

Third Party Goods means goods or services supplied by a Third Party Supplier that may be purchased through the App or Web Portal using your Afterpay Account.

Third Party Supplier means our third party supplier of Third Party Goods for whom we act as agent when processing Orders for the Third Party Goods.

Web Portal means the web-based application where we make certain features of our Afterpay Account available to you, via www.secure-afterpay.com.au.

Website means www.afterpay.com and any other website operated by Afterpay.

you or your means the person identified when an Afterpay Account is created. If:

then you or your means the person who clicks to accept the Credit Contract.

14.2. Interpretation

Shop Latitude Interest Free with a Latitude Gem Visa Credit Card** Available Instore and Online

Why Latitude interest free?

- Flexible long-term payment options

- Pay off your balance any time

- No deposit

- Shop again with Latitude Interest Free up to your approved credit limit!

How does it work?

- Add your items to your cart and checkout as normal.

- Select Latitude Interest Free as your payment method.

- Select an Interest Free plan and use your card or account number to complete.

Apply Online:

Apply for Latitude Gem Visa now and if approved, start shopping Interest Free. You’ll receive a response in under 60 seconds.Apply Now

Already have one of these cards?

Great news! You can shop using these cards in-store or online. Simply visit your nearest Amart store or select Latitude in cart.

**Excludes account service fees.

⌂ Offer ends 30/06/2025. Customers must have a valid email address to receive the Amart gift card. Valid on new Amart purchases only (not eligible on existing orders). The order must be placed in one transaction and approved within the promotional period. Spend of $1000 gets a $50 gift card, spend of $2000 gets a $100 gift card, spend of $3000 gets a $200 gift card, spend of $4000 gets a $300 gift card, spend of $5000 gets a $500 gift card, spend of $8000 gets an $800 gift card, spend of $10,000 gets a $1000 gift card. Amart Gift Card will be supplied upon completion of the order. Offer valid for online and in store purchases with Latitude Gem Visa, Credit Line, Latitude GO Mastercard and Buyer's Edge.